Inside America’s Gas Rush

Data centres, turbine queues, and the new cost of reliability

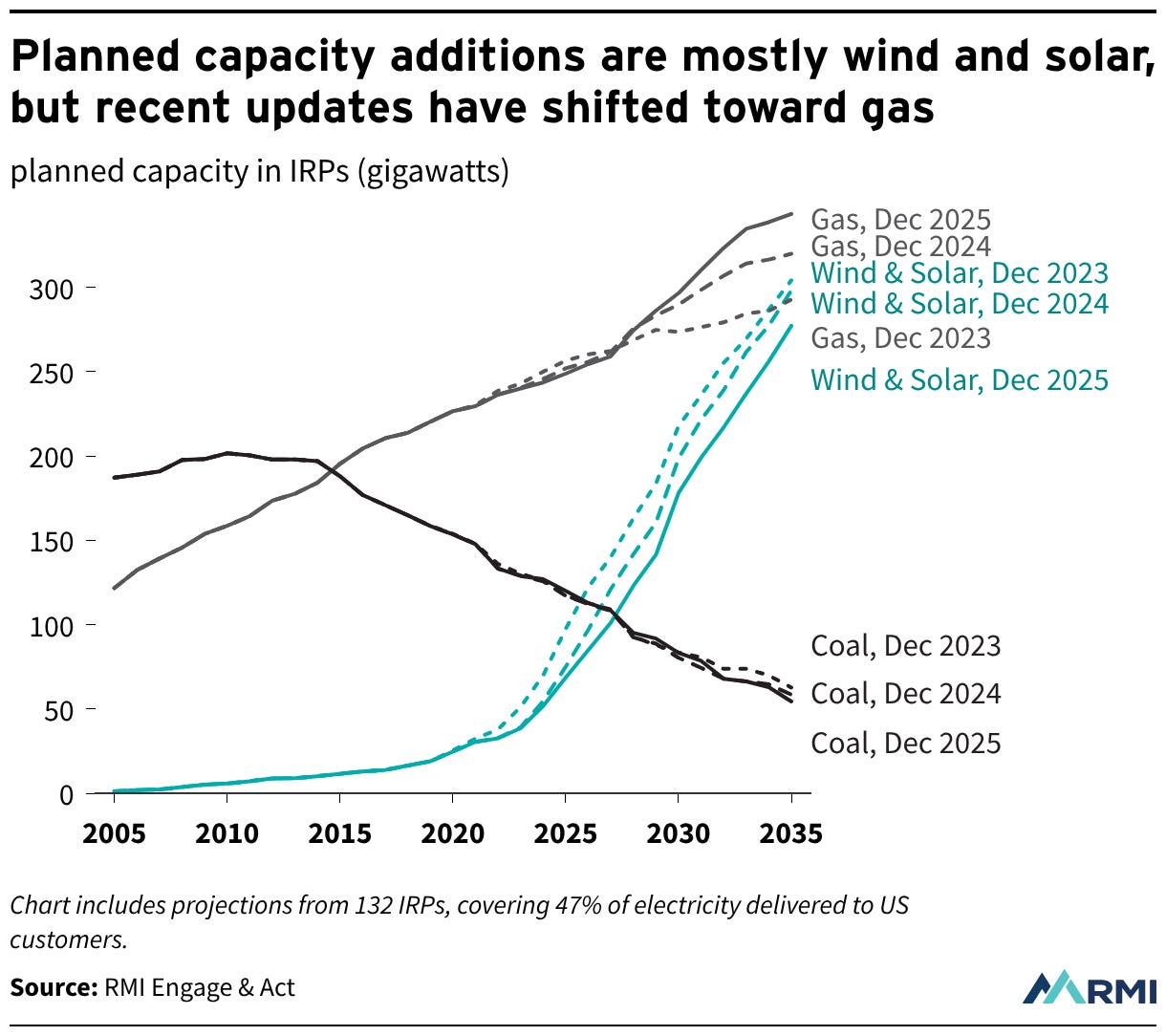

BloombergNEF’s latest gas-plant cost signal is striking: US combined-cycle gas plant project costs rose to about $2,157/kW in 2025, up from less than $1,500/kW in 2023. Bloomberg’s reporting also notes that US utilities filed for almost 24GW of gas-fired capacity in 2025, a sharp jump from 2023, while build times increased by around 23%.

At first glance, this looks like the obvious market response to rising electricity demand. Data centres, new factories, electrification, coal retirements and stretched grids all make firm capacity more valuable. Gas is dispatchable, familiar to utilities, and easier to underwrite than many still-emerging alternatives. In that narrow sense, more gas is not surprising.

But that is not the full story. The more interesting point is that the supposedly practical fallback is now showing constraint symptoms of its own: turbine queues, labour pressure, interconnection delays, pipeline questions, financing strain and ratepayer politics. Gas may still be useful. It may even be necessary in specific nodes. But usefulness is not the same as cheapness, speed or clean cost allocation.

1. The headline cost increase is real enough to matter, but it is not a single-cause story

The 66% figure should not be read as pure turbine inflation. A higher average $/kW can reflect project mix, location, size, permitting complexity, EPC scope, grid interconnection, pipeline-related works, emissions controls and financing assumptions. In other words, the average plant being filed in 2025 may not be directly comparable to the average plant filed in 2023.

Still, the direction is hard to dismiss. Independent market signals point the same way. Reuters reported that planned US gas-fired capacity more than tripled to 252GW in 2025, while combined-cycle capital costs have moved above $2,400/kW and turbine lead times have extended beyond five years. Wood Mackenzie has also described a severe gas-turbine supply-demand imbalance, with turbine prices expected to rise sharply through 2027 as developers try to secure equipment for projects tied to electrification and data-centre demand.

2. Gas still answers the reliability question better than most single alternatives

There is a reason utilities are reaching for gas. Solar and wind may provide low-cost energy, but they do not by themselves provide the same dependable capacity value at the hour and node of need. Four-hour batteries are valuable for peak shifting, reserves and short-duration flexibility, but they do not fully replace multi-day firm generation. Nuclear uprates, geothermal, long-duration storage, demand response and transmission can all help, but each has its own scale, timing and permitting constraints.

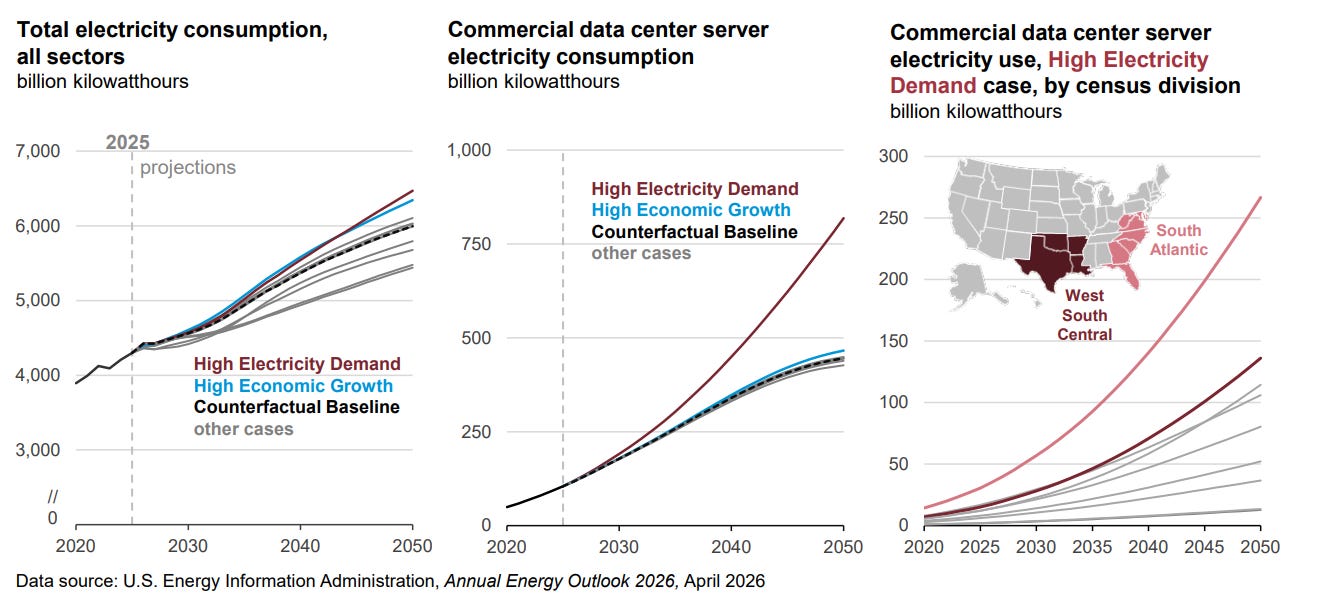

That matters because US electricity demand is no longer flat. The EIA expects US electricity use to rise for four consecutive years for the first time since 2007, with the strongest four-year growth period since 2000, driven heavily by large computing centres. In its 2026 outlook, EIA also describes data-centre load as the dominant driver of long-term US electricity growth after a decade-plus demand plateau.

The data-centre numbers explain why the system is reaching for firm capacity. Lawrence Berkeley National Laboratory estimated that US data-centre electricity consumption rose from about 58TWh in 2014 to about 176TWh in 2023, and could reach roughly 325TWh to 580TWh by 2028. That would be a very large new load wedge for a system that had spent much of the previous decade planning around modest demand growth.

3. The bottleneck has moved from electrons to deliverable capacity

The United States is not simply short of annual generation. It is short of deliverable capacity in the places and timelines where load is arriving. That distinction matters. Energy can be abundant in aggregate while reliability remains scarce at specific nodes, hours and interconnection points.

The turbine market makes the point clearly. According to Reuters, developers are ordering earlier, reserving equipment before final project certainty, using different turbine classes and considering gas engines as a bridge because large-frame turbine supply is tight. GE Vernova’s recent results tell the same story from the supplier side: strong demand for gas turbines and grid infrastructure lifted its outlook, with backlog reaching $163bn and expectations of at least 110GW of turbine backlog and reservations by year-end.

That is why “gas is fast” now needs qualification. Gas can be faster than a new nuclear plant or a major greenfield transmission build. But that does not make it unconstrained. If equipment lead times push delivery toward the early 2030s, then gas is not just the practical option; it is another infrastructure supply chain competing for scarce equipment, labour and grid access.

4. The geography matters more than the national capacity number

A national 24GW figure hides different local stories. New gas is most valuable where load growth is concentrated, transmission is constrained, coal retirements are material, or data centres require high-availability power. A plant replacing retiring capacity is not the same as a plant built around new data-centre load, and neither is the same as defensive utility reliability planning.

The current US map is not evenly distributed. Bloomberg’s project map points to clustering across the Midwest, Southeast, Texas-adjacent regions and parts of the East. Recent company updates reinforce that the demand shock is localised: NextEra has discussed large gas-fired data-centre power projects in Pennsylvania and Texas that could total nearly 10GW, while CenterPoint has cited more than 12GW of committed industrial load and plans to deliver 8GW of electric service to Greater Houston projects by 2029.

Texas shows the interaction between load, transmission and local reliability. Reuters recently reported that ERCOT supply margins are expected to remain squeezed until grid expansions arrive, with major transmission additions not expected until after 2030. That creates a near-term window in which gas looks attractive not because it is universally optimal, but because it can be sited near demand or near gas infrastructure while transmission catches up.

A better way to classify the gas buildout

5. The real political fault line is cost allocation

Higher gas capex becomes politically explosive when the cost is socialised. In a regulated utility model, capital invested in plant and equipment can enter the rate base. Customers then pay for depreciation and an allowed return through rates, subject to regulatory approval. NARUC materials describe the core ratemaking logic: a return is provided on rate base, and the cost of capital is multiplied by rate base to determine the revenue requirement recovered from customers.

That is why the type of gas project matters. If a plant replaces retiring system capacity, broad cost recovery may be defensible. If a plant is built primarily because a cluster of data centres or industrial loads arrives faster than the grid can absorb, then the allocation question becomes much sharper. Are households and small businesses paying for system reliability, or are they underwriting the backup capacity of a concentrated new load class?

This is not a theoretical problem. Policymakers and regulators are already debating how large loads should interconnect and how costs should be assigned. The Department of Energy has framed data-centre electricity demand as a major near-term system issue, while EPRI estimates that data centres could grow to consume up to 9% of US electricity generation annually.

6. Gas can lower adequacy risk while raising affordability and fuel-risk exposure

New gas can reduce blackout risk. It provides dispatchable capacity, improves reserve margins and gives system operators a controllable resource. That is valuable in a system facing fast load growth, interconnection backlogs and uncertain demand geography.

But reliability risk is not the only risk. New gas also brings fuel-price exposure, pipeline dependence, emissions risk, stranded-asset risk and bill risk. If the plant is rate-based, customers may carry the capital cost. If gas prices rise, customers may also carry fuel adjustment costs. If demand forecasts disappoint or data-centre load proves more flexible or migratory than expected, the system may be left with long-lived assets built around a temporary or overstated demand shock.

This is the trade-off the headline cost number forces into the open: gas may remain the most bankable firm-capacity tool in many US regions, but the full cost of using it is no longer just a fuel-cost question. It is a capital-cost, deliverability and allocation question.

The better question

The gas rush should not be analysed as one national story or as a simple fuel-choice debate. The useful lens is more specific: what constraint is each project solving, how deliverable is it, and who ultimately carries the cost?

That means asking:

Is the project replacing retiring capacity, serving concentrated new load, relieving a local grid constraint, or being built as defensive planning against uncertain forecasts?

Is gas still the lowest-regret firm-capacity option once dependable capacity value, build time, fuel risk, emissions exposure and local network constraints are compared properly?

Can the plant actually be delivered on the timeline implied by the demand forecast, or is the “fast” option already running into its own queue?

Who created the incremental need, and does the tariff, contract or rate-base structure allocate the cost to the customers driving it?

Which risks are being reduced ( adequacy, reserve margin, local reliability), and which risks are being shifted onto customer bills, such as capex recovery, fuel volatility and stranded-asset exposure?

Conclusion: the fallback option is being repriced

The BloombergNEF cost signal should not be read as an argument that new gas is irrational. In many US regions, gas will still be part of the practical answer to near-term reliability needs. It is dispatchable, familiar, financeable and often easier to site than alternatives that require large new transmission, long-duration storage or still-scaling technologies.

But the same signal does challenge the simplistic version of the gas argument. Gas is not magically outside the infrastructure economy. It needs turbines, skilled labour, permits, pipelines, interconnection, financing and regulatory approval. When everyone reaches for it at once, those inputs become scarce and their cost rises.

The final lesson is therefore more precise than “build more gas” or “do not build gas”. The US power system is being forced to distinguish between energy, capacity and deliverability. The question is not just how much generation is added, but whether the right kind of firm capacity is built in the right places, on the right timeline, and paid for by the right customers.

Gas can still reduce adequacy risk. But if expensive new gas is built for concentrated demand and recovered broadly through customer bills, reliability risk falls while affordability and allocation risk rise. That is the real analytical fault line.

References and source notes

2. EnergyNow syndicated summary of BloombergNEF gas-plant cost figures.

3. Reuters, “Power developers adapt gas turbine strategies to mitigate tight supply” (2 March 2026).

4. Wood Mackenzie, “Gas turbine prices soar 195% as market faces supply-demand crisis” (1 April 2026).

6. US EIA, Annual Energy Outlook 2026 release (8 April 2026).

7. Lawrence Berkeley National Laboratory / DOE, 2024 United States Data Center Energy Usage Report.

8. Reuters, “GE Vernova lifts 2026 outlook as AI boom fuels power equipment demand” (22 April 2026).

11. Reuters, “Texas power supply margins squeezed until grid expansions kick in” (21 April 2026).

12. NARUC, Revenue Requirements, Rate Base and Cost of Capital.

US Department of Energy, Clean Energy Resources to Meet Data Center Electricity Demand.